5. What’s in this for investors?

So far, evidence suggests that there’s little difference in the performance of green and traditional bonds. There is, however, an increasing body of research suggesting that investment strategies that focus on ESG goals do better, probably because they screen out poorly run firms. So far, the rise of green loans hasn’t led to higher funding costs for companies in the extractive industries, but the idea that investor sentiment or government policies might drive up their funding costs has become an active if longer-term worry.

6. Who decides what’s really green?

So-called greenwashing is still a risk, and critics complain about a lack of global standards and inconsistency among ESG scoring methods. The European Union’s June 2019 proposals for a green-bond standard and verification system are seen as potentially creating a benchmark that could ease the sale of green securities worldwide (Bloomberg provides ESG data).

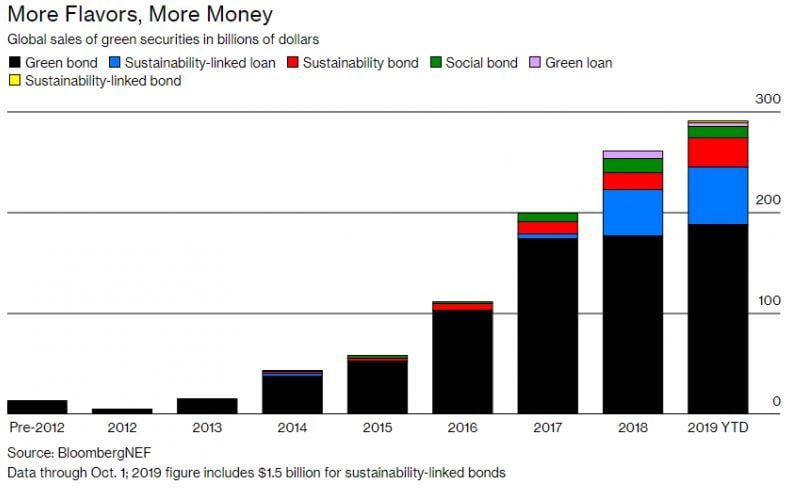

7. Where is green lending happening?

China’s green bond market has rushed ahead as part of the government’s effort to limit air pollution. Scandinavian investors and French lenders such as BNP Paribas and Credit Agricole have been prominent among the pioneers in this sector; U.S. investment banks now sense they need to compete. Countries with emerging economies such as Indonesia and Nigeria that are short of capital argue that green lending could help them build out their infrastructure in a climate-friendly way, giving a bigger bang per green buck. But they’re also where projects are most likely to fall short on transparency and other governance risk measures.