Financial market reforms and openings continue to speed ahead. The bond, equity and foreign exchange markets are growing, presenting more opportunities for global investors. All of which may be why last summer, 40 percent of attendees at a Bloomberg buy-side conference indicated they are “more likely” to invest in emerging markets or North Asia in the next 12 months.

Will the trade war end or escalate?

Hanging over China’s investment prospects, however, is the uncertainty of the ongoing trade war with the U.S. An agreement between the two nations to reduce trade tensions is a positive sign for China’s growth, but it is not yet clear that its economy is out of the woods.

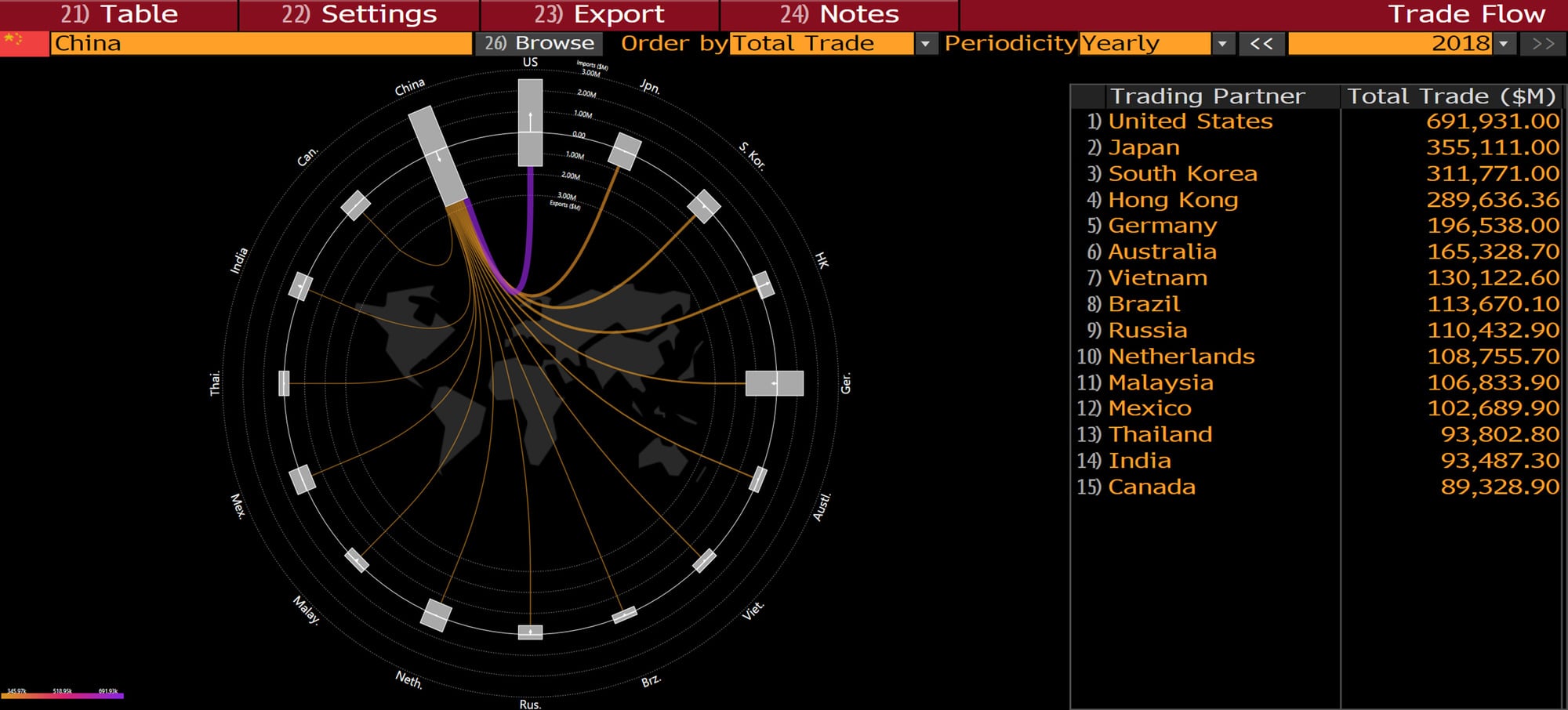

China total trade in 2018 by country

“The short-term outlook for 2019 is not especially great,” says Chang Shu, chief Asia economist for Bloomberg Economics. “The domestic economy is declining. The trade war is creating a lot of uncertainty. If there is more external pressure, the government will crank up investment, potentially generating more debt and creating more financial risks in the medium term. If trade tension eases, we may still see some slowdown but better overall composition of growth.”

Shu describes three potential scenarios for how the trade situation could affect China’s growth.

The first is true de-escalation, which could lead to China’s growth slowing to 6.3 percent from 6.6 percent for 2018, while exports slow slightly to 7 percent growth (down from 13.7 percent in 2018) and investment increasing 8.2 percent. The second scenario assumes the U.S. tariff rates rise to 25 percent in March, with growth slowing to 6.2 percent, exports declining by 3.9 percent and investment rising 11.1 percent. The third (and most unlikely) scenario assumes even higher tariffs on a wider range of imports, a situation in which growth slumps to 5.9 percent.

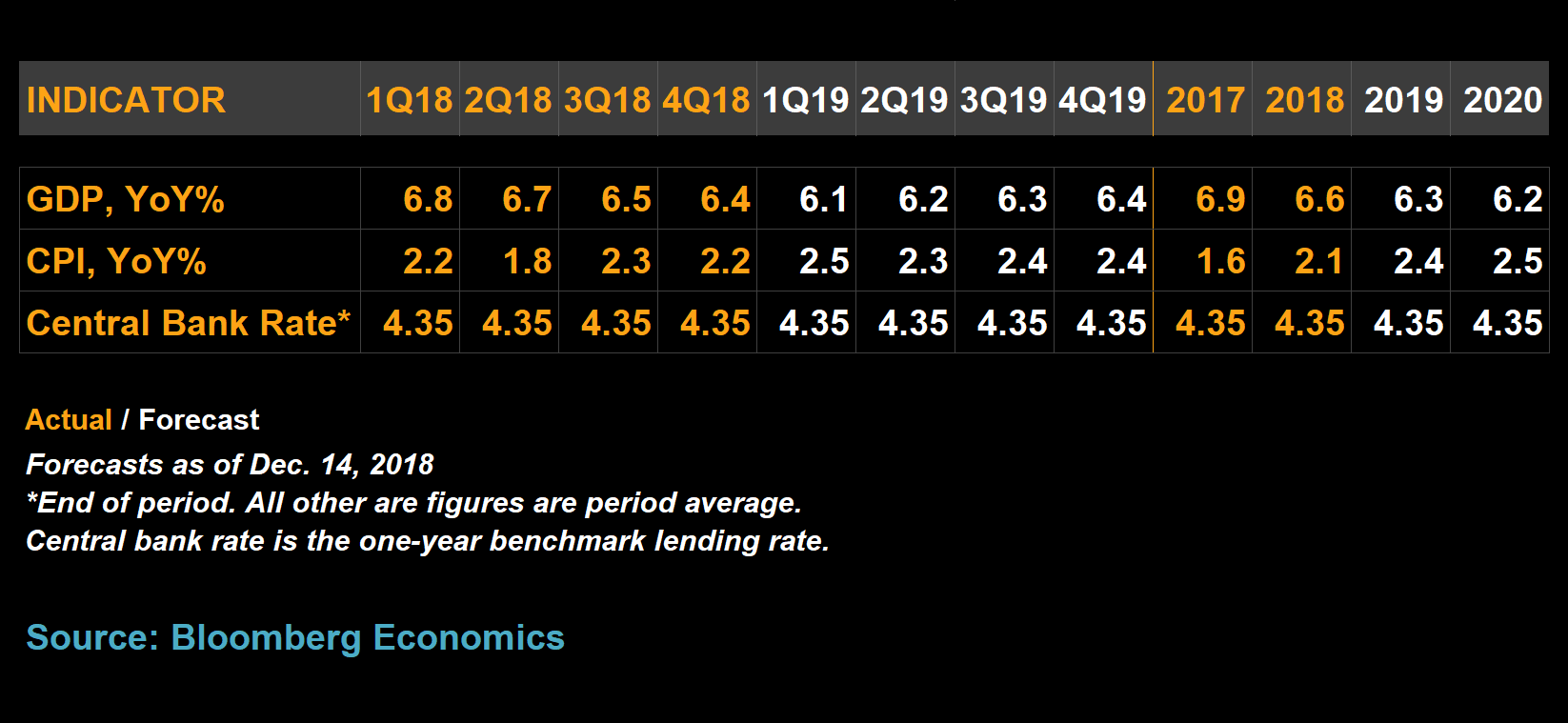

China economic forecast table

Domestically, Shu sees other risks, pointing out that many of the country’s key long-term policy goals — such as deleveraging, environmental regulation and control of government financing — involve growth trade-offs.

“Supporting growth without abandoning deleveraging and reforms is a lot harder to pull off than another major stimulus,” she says. “With leaders reluctant to give up hard-won progress necessary to sustain the economy in the medium term, stabilization in growth could take longer.”

Evaluating opportunities

Given these dynamics, how should the buy side evaluate opportunities in China in 2019? Is it fundamentally different from other geographies, or should asset managers still go sector by sector, company by company, security by security?

“Overall, China is quite similar to many other emerging markets in its patterns,” Shu says. “What makes it different is its size. If your risk is at a one in other emerging markets, for example, that risk will have a much larger multiplier in China.”

Shu notes there is a definite push and pull of financial opening followed by the government’s doubts about the opening, leading to constant swings in policy. She points to exchange rates to illustrate this idea. When the yuan declined recently, for example, the People’s Bank of China (PBOC) implemented a number of tools reminiscent of a time when it had much more stringent control, including stronger daily fixing rates, regulatory measures and window guidance.

“This helped the yuan, but with a slowing economy, potential trade war and generally negative sentiment about emerging markets, the downward pressure is likely to persist,” Shu says. “In other words, the PBOC may need to keep using this old playbook, which means its longer-term goal of capital account liberalization will get pushed to the back burner.”

Local perspective

While leadership has been making pro-growth changes since last June, macro data indicates the impact hasn’t yet arrived. Anecdotal evidence suggests the same — that private companies aren’t feeling much support from new policies yet. After a two-week trip to Beijing and Shanghai, Shu notes that private companies seem starved of funding and sentiment is weak.

“There’s a big risk that tight liquidity and poor sentiment deter private investment, dragging down growth and worsening the mix,” she says. “Tackling those challenges is crucial to re-energizing the private sector. The payoff would be stronger growth and a recovery that’s more balanced, with less reliance on government-led infrastructure spending and associated debt.”

During her trip, Shu encountered small and medium-sized private companies under stress due to tight liquidity in both traditional segments, such as footwear, as well as new ones, such as medical services. Cut off by trust companies, these firms are having real trouble finding alternative sources of funding. More to the point, assets in the shadow banking sector declined by 3 trillion yuan from a peak at the start of 2018, pain that is felt primarily by smaller private firms — a fact that is spreading pessimism across the private sector according to the firms Shu spoke with.

Looking ahead

This is not to say that 2019 lacks opportunity. Shu feels positive about the Chinese insurance sector heading into 2019, along with construction, construction materials, transportation and related companies, because the government will likely continue to support infrastructure projects. Technology companies are another potential bright spot, including manufacturers as well as those developing new applications, such as AI in entertainment.

“Overall, there are positive developments in China,” Shu says. “The more the equity and bond markets grow, the more the country opens to global investors, the more promise there is for more efficient allocation of capital. But there is still a long road ahead.”

Looking even further ahead than 2019, Shu and her team at Bloomberg Economics estimate that Chinese stocks held by foreign investors could grow six times by 2025, and bonds close to 16 times.

“These estimates reflect forecasts for what China could achieve if reform and opening stay on track and there’s no significant setback in growth,” she says. “Critical to this success is a consistent approach that alleviates fears of sudden policy reversals.”

The Bloomberg Terminal's RMB bond solutions and Bond Connect transform the liberalization of China's bond markets into actionable opportunity. Connect instantly to onshore market players, gain unrivaled transparency into China bond prices and use custom analytics to power success in this multi-trillion dollar market. Learn more.